The role of insurance in therapy: your 2026 guide

- 2 days ago

- 8 min read

TL;DR:

Insurance in therapy helps cover health treatment costs, making mental health care more accessible.

Insurance plans typically require a documented clinical diagnosis for coverage and support outpatient services.

Insurance in therapy is defined as the financial mechanism by which health insurers cover the cost of mental and physical health treatment, reducing what patients pay out of pocket. The role of insurance in therapy extends beyond simple reimbursement. Under the Mental Health Parity and Addiction Equity Act (MHPAEA), insurers must apply the same coverage standards to mental health treatment as they do to physical health care. That legal requirement means therapy is no longer a luxury reserved for those who can afford full private fees. Understanding how your policy works, what it covers, and where the gaps lie is the difference between affordable care and an unexpected bill.

What does insurance typically cover in therapy?

Most major health insurance plans now cover behavioural health services, including outpatient therapy, counselling, and psychiatry, provided two conditions are met: the therapist holds a recognised clinical licence, and the patient has a documented diagnosis. That second condition matters more than most patients realise. Insurance does not pay for general wellbeing support. It pays for medically necessary treatment.

Covered services generally include:

Outpatient individual therapy with a licensed psychologist, psychotherapist, or clinical social worker

Psychiatric consultations for assessment and medication management

Cognitive Behavioural Therapy (CBT) and other evidence-based psychological treatments

Physiotherapy and musculoskeletal rehabilitation when prescribed following injury or surgery

Group therapy sessions led by a licensed provider in a clinical setting

Physical therapy and mental health therapy are treated differently in one important respect. Physical therapy coverage tends to be straightforward: a GP referral, a diagnosis, and a course of treatment. Mental health therapy requires the same documented diagnosis, but parity rules under MHPAEA prohibit insurers from applying more restrictive limits to mental health than to comparable physical health services.

Many reasons people seek therapy, such as grief, relationship difficulties, or general stress, do not meet the threshold for a billable clinical diagnosis. Insurance denies payment for non-diagnosable conditions. A therapist cannot fabricate a diagnosis to satisfy billing requirements. Doing so constitutes fraud with serious legal consequences. Patients seeking support for life challenges without a clinical condition will need to fund those sessions privately.

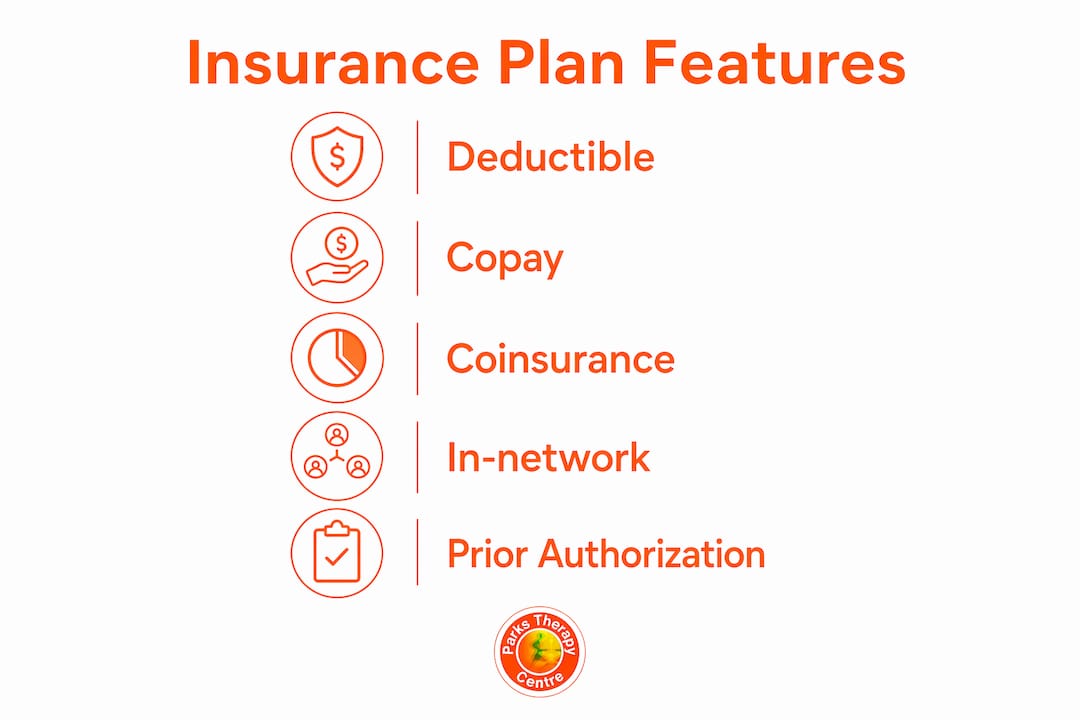

How do insurance plan features affect therapy costs?

The structure of your insurance plan determines how much you actually pay per session. Three features drive the majority of out-of-pocket costs: the deductible, the copay, and coinsurance.

Feature | What it means | Typical range |

Deductible | Amount you pay before insurance contributes | £200–£1,500+ per year |

Copay | Fixed fee per therapy session | £15–£50 per session |

Coinsurance | Your percentage share after the deductible | 20%–40% per session |

Out-of-network cost | Higher share when using non-panel providers | Often 50%+ of session cost |

In-network providers have agreed rates with your insurer. Out-of-network providers charge their own fees, and your insurer covers only a portion, if anything at all. Only approximately 43% of private therapists accept new patients with insurance. That figure reflects low reimbursement rates and administrative burden on therapists, not a shortage of qualified practitioners. The practical consequence is that even patients with good coverage may struggle to find an in-network therapist quickly.

Adults attending therapy frequently should seek plans with out-of-network deductibles below £1,500 and coinsurance at around 30% or better. Higher-tier plans, equivalent to Marketplace “Gold” plans in the United States, typically deliver better value for regular therapy users than lower-premium plans with high deductibles.

Prior authorisation is another barrier. Some insurers require approval before covering ongoing therapy sessions. Parity law forbids stricter authorisation standards for mental health than for comparable medical services. If your insurer demands more paperwork for therapy than for a specialist medical appointment, that may constitute a parity violation worth challenging.

Pro Tip: Ask your insurer specifically whether prior authorisation applies to your therapy and, if so, how many sessions are approved per request. Getting this in writing prevents disputes mid-treatment.

What are the privacy implications of using insurance for therapy?

Using insurance for therapy creates a clinical paper trail. Insurance requires a documented diagnosis to authorise and reimburse sessions. That diagnosis, along with session notes documenting your progress and treatment goals, becomes accessible to your insurer as a third party with legal audit rights. This is not a theoretical concern. Insurers do review clinical notes to verify medical necessity.

The key privacy considerations are:

Diagnosis on record: A formal mental health diagnosis becomes part of your permanent health record and may be visible to future insurers.

Session note access: Therapy notes documenting what you discuss can be reviewed by insurer auditors, not just billing codes.

Third-party disclosure: Your therapist is legally required to share records with the insurer upon request when you are using insurance to pay.

Employment implications: In some contexts, a mental health diagnosis on your health record may be relevant to occupational health assessments.

Some adults prefer paying privately to avoid creating a permanent diagnosis record. Private pay means no insurer involvement, no audit rights, and no diagnosis requirement. The trade-off is the full session cost, which varies widely by provider and location.

Pro Tip: If privacy is a concern but cost is also a factor, ask your therapist whether they offer a sliding scale fee for private-pay patients. Many do, and the rate may be closer to your insurance copay than you expect.

For patients considering physiotherapy insurance cover, the documentation requirements are similar but the privacy stakes tend to be lower, as musculoskeletal diagnoses carry less social stigma than mental health diagnoses.

What practical steps can patients take to verify therapy benefits?

Verifying your insurance benefits before your first session prevents the most common and costly surprises. Real-time benefit verification directly with your insurer is the single most effective step you can take before starting therapy.

Call your insurer directly. Ask specifically about behavioural health or mental health benefits, not just general health cover. Request confirmation of your deductible, copay, coinsurance, and session limits in writing or by email.

Confirm your therapist is in-network. Provider directories are often out of date. Call the therapist’s practice and ask them to confirm your specific plan is accepted before booking.

Ask about out-of-network benefits. If no in-network therapist is available, find out whether your plan includes out-of-network reimbursement and at what rate.

Check for prior authorisation requirements. Ask how many sessions are covered without a new authorisation request and what the renewal process involves.

Enquire about Employee Assistance Programmes (EAPs). Many employers offer EAPs that provide a set number of free therapy sessions per year, entirely separate from your health insurance. These are frequently underused.

Consider sliding scale and community options. If insurance does not cover your preferred therapist, sliding scale fees, community mental health centres, and university training clinics offer lower-cost alternatives.

Know how to appeal a denial. If a claim is denied, you have the right to appeal. Parity law violations are a valid grounds for appeal if your mental health claim faces restrictions not applied to equivalent physical health claims.

Lack of awareness about payment pathways, including in-network, out-of-network, EAPs, and sliding scale options, is one of the most significant barriers to therapy access. Knowing all four options before you start gives you real negotiating power. When selecting a clinic, guidance on choosing the right physiotherapy clinic applies equally to mental health providers: check credentials, confirm insurance acceptance, and ask about cancellation policies before committing.

For patients managing ongoing physical rehabilitation, understanding insurance cover for physiotherapy in 2026 can reveal supplementary cover options that reduce costs further.

Key takeaways

Insurance in therapy is most effective when patients understand their plan’s structure, verify benefits before starting treatment, and know their rights under parity law.

Point | Details |

Parity law protects patients | MHPAEA requires mental health coverage to match physical health coverage in cost and access. |

Diagnosis is required for cover | Insurance only pays for therapy tied to a documented clinical diagnosis, not general wellbeing support. |

Plan structure drives real costs | Deductibles, copays, and in-network status determine what you actually pay per session. |

Privacy is a genuine consideration | Insurers have legal audit rights over clinical notes; private pay removes this third-party access. |

Verify before you book | Confirming benefits directly with your insurer before the first session prevents unexpected costs. |

What most patients miss about insurance and therapy

The conversation about insurance and therapy tends to focus on whether coverage exists. The more useful question is what the coverage actually delivers in practice. Parity law is a genuine protection, but it does not guarantee a short waiting list or a therapist who accepts your plan. Only 43% of private therapists accept new insurance patients, which means having coverage and finding someone who accepts it are two separate problems.

The privacy dimension also catches people off guard. Most patients assume that what they say in therapy stays between them and their therapist. When insurance is involved, that assumption is incomplete. Insurers have legal rights to audit clinical notes, and a formal diagnosis becomes part of your health record. That is not a reason to avoid insurance, but it is a reason to make an informed choice rather than a default one.

The practical advice I give anyone starting therapy is this: spend twenty minutes on the phone with your insurer before you book a single session. Ask every question on the verification list. Then ask your therapist’s practice to confirm your plan directly. The gap between what your insurer says is covered and what your therapist’s practice can actually bill is where most billing surprises live.

EAPs remain the most underused resource in this space. Many adults have access to six or more free therapy sessions through their employer and never use them because they do not know the benefit exists. Check your employee handbook or ask your HR department before spending anything on therapy.

— Ivan

Therapy at Parkstherapycentre: insurance accepted, no surprises

Parkstherapycentre has provided physiotherapy, sports injury treatment, acupuncture, podiatry, and related therapies across Bedfordshire and Buckinghamshire since 1986. The centre accepts insurance cover and works with patients to clarify what their plan includes before treatment begins.

If you are ready to start treatment and want to understand your cover first, Parkstherapycentre’s team can guide you through the process. Visit the Parkstherapycentre main page to book online, check service options, and confirm whether your insurer is accepted. Clear information before your first session means you can focus on recovery, not paperwork.

FAQ

Does insurance cover therapy for mental health?

Most major health insurance plans cover mental health therapy, including counselling and psychiatry, when a licensed provider documents a clinical diagnosis. The MHPAEA requires mental health coverage to be comparable to physical health coverage.

What is the cost of therapy with insurance?

The cost of therapy with insurance typically includes a copay of £15–£50 per session after your deductible is met. Exact costs depend on your plan tier, whether your therapist is in-network, and any coinsurance percentage that applies.

Does insurance cover therapy for grief or relationship issues?

Insurance generally does not cover therapy for grief or relationship difficulties unless a formal clinical diagnosis is documented. Non-diagnosable conditions are excluded from insurance billing, meaning patients pay privately for these sessions.

Can my insurer read my therapy notes?

Yes. When you use insurance to pay for therapy, your insurer has legal audit rights over clinical notes to verify medical necessity. Patients who want to keep session content fully private may choose to pay privately instead.

What should I do if my therapy claim is denied?

Request a written explanation of the denial and check whether the restriction applied to your mental health claim would also apply to a comparable physical health service. If not, the denial may violate parity law and you have grounds to file a formal appeal with your insurer.

Recommended